Kospi breaks records — but is the ‘Korea discount’ really over?

Published: 02 Oct. 2025, 16:38

Updated: 02 Oct. 2025, 17:16

-

- JIN MIN-JI

- [email protected]

-

- PARK EUN-JEE

- [email protected]

![A dealer stands in Hana Bank’s dealing room in Jung District, central Seoul on Oct. 2, as the Kospi closes at an all-time high of 3,549.21, surpassing the 3,500 mark for the first time. [YONHAP]](https://koreaseafood.online/data/photo/2025/10/02/c251b894-90cc-4c0c-85ec-ccecfbf6e214.jpg)

A dealer stands in Hana Bank’s dealing room in Jung District, central Seoul on Oct. 2, as the Kospi closes at an all-time high of 3,549.21, surpassing the 3,500 mark for the first time. [YONHAP]

[NEWS ANALYSIS]

The latest market rally, first sparked by the June inauguration of President Lee Jae Myung, has renewed investor hopes that Korea’s longstanding valuation gap — the so-called Korea discount — may narrow, lifting Kospi’s valuation multiples.

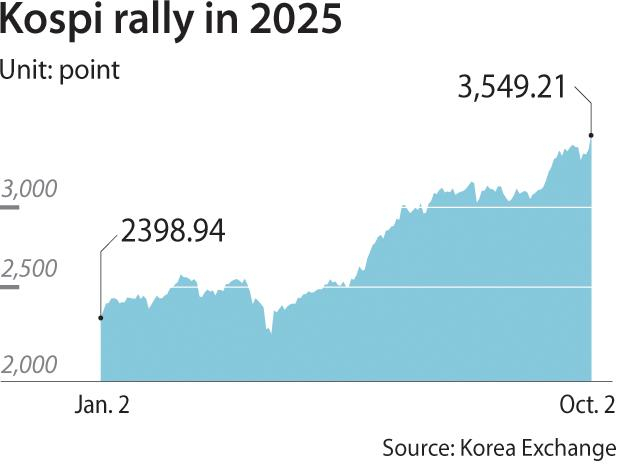

The Kospi exceeded the 3,500 mark for the first time in history on Thursday, just before the long Chuseok holiday break, to close at 3,549.21, up 2.7 percent from the previous day.

Korea’s benchmark index has jumped by 47.9 percent as of Oct. 2 from the beginning of this year despite weak economic growth. It has been fueled by falling interest rates, an AI chip boom that lifted expectations for chip exports and the Lee administration’s ambitious push to drive the index to 5,000 points.

Its price-to-earnings (P/E) and price-to-book (P/B) ratios — the two most used valuations to assess whether a stock index is undervalued — have improved following the recent rally.

The Kospi’s P/E ratio rose to 15.95 compared to 13 at the start of the year, while its P/B ratio increased from 0.84 to 1.1 over the same period. But they remain far lower than many other key nations, including the United States where the S&P 500 has a P/E ratio of around 27 and a P/B ratio of roughly 5.5.

The P/E ratio shows how much an investor is paying for each dollar of a company’s earnings, while the P/B ratio represents how much an investor is willing to pay for each dollar of the company’s net assets.

Lower ratios can indicate undervaluation of the stocks, or that investors expect slower growth or higher risk in the future.

“The Korea discount is in the process of being dismantled,” said Lee Won, an analyst at Bookook Securities. “The proposed revisions to the tax and Commercial Act are expected to further support the rally — a trend likely to continue throughout the current administration given the policies in place. However, if pushed through too hastily, they could trigger side effects and potentially stall the market’s momentum.”

Kospi's gain was especially steep in September, with the index reaching an all-time high. This pushed the year-to-date gain well beyond that of other major Asian indexes, including the Nikkei 225’s 15 percent and the HSCEI’s 30 percent.

![Jeong Eun-bo, chairman of the Korea Exchange, delivers opening remarks at the Korea Capital Market Conference hosted by the exchange at the Westin Josun Hotel in central Seoul on Sept. 29. [YONHAP]](https://koreaseafood.online/data/photo/2025/10/02/ac7958ab-838e-4e72-9d41-8e97e808c9a6.jpg)

Jeong Eun-bo, chairman of the Korea Exchange, delivers opening remarks at the Korea Capital Market Conference hosted by the exchange at the Westin Josun Hotel in central Seoul on Sept. 29. [YONHAP]

“The Kospi’s valuations are steadily improving, helping to overcome the longstanding Korea discount,” said Jeong Eun-bo, the chairman of the Korea Exchange (KRX) during a conference on Korea’s capital market on Sept. 29. He added that the market is undergoing reassessment and pledged to foster a market environment that establishes the Korea premium as the new normal.

Some brokerages project that the index could advance further, with JP Morgan forecasting it to surpass 4,000 in the next 12 months.

Still, downside risks remain. For instance, the Democratic Party’s push to mandate listed companies to cancel treasury shares — part of the third revision to the Commercial Act — could rapidly deplete their excess cash, leaving fewer funds available for investment. That, in turn, could impact on a company’s competitiveness, and ultimately, its stock price, Lee added.

There are also several uncertainties that need to be addressed — including the U.S. tariffs and questions surrounding how Korea will finance the $350 billion investment pledged to the United States in return for lower rates for “reciprocal” tariffs.

Industry insiders note that, depending on the financing method, the investment could trigger a sudden outflow of U.S. dollars. The shift may lead to volatility in the won-dollar exchange rate, which investors would likely interpret as a source of uncertainty.

Some argue that it is too early to draw any conclusions about the end of the Korea discount based on the latest rally.

“The Korea discount is linked to fundamental issues, such as corporate governance and transparency in stock trading,” said Won Jai-hwan, a finance professor at Sogang University. “These issues take time to resolve, so it’s too early to discuss the Korean stock market’s transition from being discounted to heading toward achieving a premium.”

The recent surge in Kospi, supported by market-friendly policies, is laying groundwork for companies to build up momentum to drive the index’s growth.

“Looking at the case of Japan, policies were introduced first, followed by the involvement of activist funds and the implementation of regulations from the exchange,” said Hwang San-hae, an analyst at LS Securities. “Only after that did companies start to change their behavior. I see that we are currently building that kind of foundation.”

BY JIN MIN-JI, PARK EUN-JEE [[email protected]]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)