Shin Hyun-song’s playbook: How new BOK chief diverges from his predecessor

Published: 21 Apr. 2026, 14:59

Updated: 21 Apr. 2026, 19:44

-

- JIN MIN-JI

- [email protected]

![Bank of Korea's new governor Shin Hyun-song gives an inaugural address at the central bank in central Seoul on April 21. Shin signaled a more flexible approach to monetary policy in the speech amid geopolitical uncertainty in the Middle East. [BOK]](https://koreaseafood.online/data/photo/2026/04/21/b72358e8-d2b2-40fd-944e-5e4c0d8326ee.jpg)

Bank of Korea's new governor Shin Hyun-song gives an inaugural address at the central bank in central Seoul on April 21. Shin signaled a more flexible approach to monetary policy in the speech amid geopolitical uncertainty in the Middle East. [BOK]

[KEY PLAYER]

Shin Hyun-song’s arrival as governor of the Bank of Korea (BOK) is poised to reshape Korea's monetary policy direction, with investors watching for a shift away from easing and a reassessment of the forces driving the won’s weakness. His communication style — expected to be more principle-based and less activist than that of his predecessor — is also attracting scrutiny.

As war-driven inflation and an energy shock intensify, markets expect the Oxford-educated economist to end the rate-easing cycle and take a more targeted approach to tame the weak won, as he points to offshore nondeliverable forwards (NDF) and the U.S. rate gap as key drivers of its weakness in contrast to his predecessor Rhee Chang-yong’s emphasis on retail overseas investment flows.

“Uncertainty over the paths of inflation and growth has increased further due to supply shocks stemming from the war in the Middle East, and monetary policy should be conducted in a cautious and flexible manner to safeguard price and financial stability,” Shin said at his inauguration on Wednesday, as he outlined the BOK’s four key priorities.

These also include strengthening its early-warning system by making more active use of market price indicators to assess financial soundness, as well as plans to build monetary infrastructure to support the internationalization of the won and to design a future monetary framework in response to digital financial innovation.

Shin, the first Asian scholar to serve as an economic adviser and head of research at the Bank for International Settlements (BIS), also stressed the importance of the BOK’s role in structural reform challenges, including Korea’s demographic shift, widening inequality and elevated household debt.

“The structural issues are key variables that shape the operating environment for monetary policy. As the structure of the economy changes, a widening gap between economic reality and the perceptions of economic agents can also affect the transmission channels of monetary policy.” Shin added, “In this sense, I view structural factors not as separate from monetary policy, but as an important part of its operating framework.”

An alleged pragmatic hawk

While Shin struck a broadly neutral tone at his confirmation hearing, he is widely viewed as a hawkish economist who has called for pre-emptive rate hikes.

Shin has repeatedly stressed the need to tighten policy before inflation expectations become unanchored, underscoring concerns over price pressures and financial imbalances, while Rhee has taken a more situation-dependent approach, aggressively raising rates to combat inflation but adopting a more cautious stance when shifting toward cuts.

Shin’s hawkish tone was partly witnessed during the confirmation hearing.

“Given that the Middle East crisis has not been resolved quickly, I expect price pressures will continue,” Shin said during the hearing. “If it persists over a longer period, it will feed into inflation expectations and core inflation, and ultimately broader inflation. In that case, monetary policy will certainly have a role to play.” His remarks came as import prices in March surged 16.1 percent from a month earlier, the steepest increase since 1998, driven by a nearly 90 percent jump in crude oil import prices.

His stance echoes comments in 2022, when he argued that central banks should act early and aggressively as inflation risks build, warning that delayed tightening can allow inflation to become entrenched, making it harder and costlier to bring down.

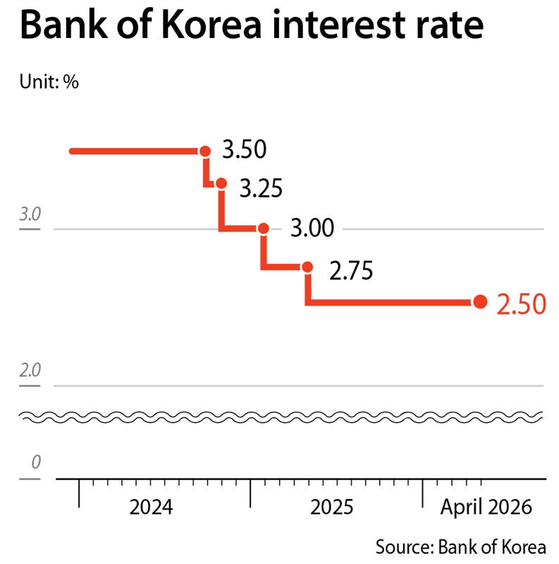

Under this policy stance, some global banks expect the BOK to raise rates multiple times this year, with Kim Jin-wook, chief economist at Citi Research Korea, forecasting in a report last week two quarter-percentage-point hikes, in July and October.

But some economists have described Shin’s remarks at the confirmation hearing as more moderate than hawkish, pointing to his characterization of the current 2.5 percent policy rate as “appropriate” and his comments that no monetary policy response would be needed if the current shock from Middle East tensions proves temporary, according to KB Securities fixed-income analyst Lim Jae-kyun.

Different diagnosis on forex

Under Rhee’s leadership, the BOK cited retail investors’ overseas trading as one of the key contributors to the persistently weak won, which has already crossed the psychologically important 1,500 level multiple times this year.

Shin, however, takes a different view. He points to offshore NDF trading in the won and the U.S.–Korea interest rate differential as key drivers of the currency’s weakness against the dollar.

“When exchange rates move sharply, as they did in March, forward transactions can have a greater impact than the overall scale of capital outflows,” Shin said, describing the situation as a “tail wagging the dog” phenomenon. “Forward foreign exchange transactions are ultimately driven by the U.S.–Korea interest rate differential,” he added, calling the gap “considerably wide.”

Shin also vowed to “make the won more widely used globally and build an offshore settlement system” to improve Korea’s ability to manage exchange-rate volatility and to strengthen the won’s international standing, as part of efforts to address its weakness.

His approach to the weak won differs from Rhee’s, who in November dismissed the Korea–U.S. rate gap as a driver of the currency’s weakness. He instead highlighted the impact of domestic capital outflows, including overseas investment by young investors and the National Pension Service.

Narrower focus on core central-bank role

The BOK is also expected to adopt a narrower, more central bank-focused communication style under its new governor.

Although Shin said in his inauguration speech that broader economic issues such as structural reforms are becoming an important factor shaping monetary policy, and pledged to engage in two-way communication with markets and coordinate policy with the government where necessary, some expect his approach to be narrower than Rhee’s based on his past remarks.

In a recent BIS Quarterly Review, Shin noted that if policymakers are not truly confident about the economy’s fundamental direction, they should not attempt to preemptively guide markets, according to Jeong Hyung-ki, an analyst at DS Investment & Securities.

Shin explained that while forward guidance can enhance the transmission of monetary policy, its continued use reduces flexibility and limits the central bank’s room for maneuver.

The approach marks a departure from Rhee’s more active communication style, which included forward guidance and a Fed-inspired dot plot reflecting board members’ rate outlooks. Rhee also frequently spoke on a broad range of social and economic issues, including the need for structural reforms to complement the limits of monetary policy, as well as sensitive topics such as university entrance exam reform and foreign labor policy.

Shin has in fact taken a somewhat ambiguous stance on the dot plot. On whether to maintain the dot plot system, he said at the hearing there is an intention to “continue operating the current framework in the near term.” He added, however, that a period is needed to assess and evaluate how the system works after its introduction in order to further refine communication.

BY JIN MIN-JI [[email protected]]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)