As Kospi enters '6,000' era, analysts project bull run to charge on

-

- PARK EUN-JEE

- [email protected]

-

- JIN MIN-JI

- [email protected]

![Financial Supervisory Service Governor Lee Chan-jin, fourth from left, Financial Services Commission Chairman Lee Eok-won, fifth from left, and Korea Exchange Chairman Jeong Eun-bo, sixth from left, along with other participants, hold a ceremony at the Korea Exchange in Yeouido, Seoul, on Feb. 25 to celebrate the Kospi surpassing the 6,000-point mark. [JOINT PRESS CORPS]](https://koreaseafood.online/data/photo/2026/02/25/f556e7a2-64e9-488e-95f7-e76ef0492f09.jpg)

Financial Supervisory Service Governor Lee Chan-jin, fourth from left, Financial Services Commission Chairman Lee Eok-won, fifth from left, and Korea Exchange Chairman Jeong Eun-bo, sixth from left, along with other participants, hold a ceremony at the Korea Exchange in Yeouido, Seoul, on Feb. 25 to celebrate the Kospi surpassing the 6,000-point mark. [JOINT PRESS CORPS]

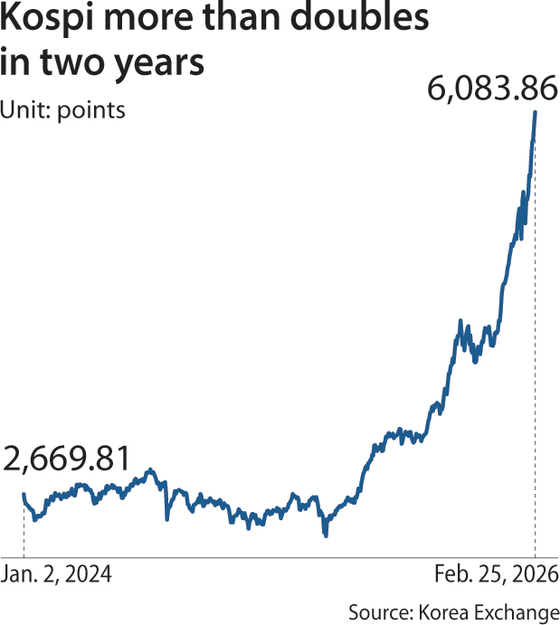

The Kospi smashed past 6,000 points on Wednesday, just a month after breaking the 5,000-point mark, defying U.S. tariff threats and fears of a potential AI bubble.

While the unprecedented gains have sparked overheating concerns, many analysts at home and abroad say the rally could extend further, potentially reaching 8,000.

The main bourse closed at a fresh high of 6,083.86 on Wednesday, up 1.91 percent from the previous trading day. The index represents a jump of more than 40 percent in just the first two months of 2026 on strong memory chip demand and a market-friendly policy push by the government, extending last year’s steep 75 percent gain.

Nomura Financial Investment has lifted its first-half bull case outlook to 8,000 points, citing strong memory-chip earnings and rising corporate value — signaling potential gains of more than 30 percent over the next four months. JPMorgan Chase also raised its bull case target to 7,500 points in early February.

While semiconductors are expected to continue driving the index, boosted by a memory chip shortage, analysts note that related sectors, such as robotics — set to benefit once hyperscalers begin monetizing AI — as well as the shipbuilding and nuclear plant industries, could provide additional support, fueling expectations that the Kospi’s gains may extend well beyond the chip market.

The Korea JoongAng Daily sat down with Jason Lui, head of APAC equity and derivatives strategy at BNP Paribas, and Kim Doo-un, senior analyst at Hana Securities, for insight on the Kospi outlook and the key factors shaping Korea’s market momentum.

Below are edited excerpts from the interview, edited for length and clarity.

Q. Multiple institutions are raising their forecasts for the Kospi, while others warn that the market may be overheating. What is your future Kospi target in the mid-to-long run?

Kim Doo-un, senior analyst at Hana Securities

A. Kim: More than 70 percent of the upward revisions to Kospi earnings forecasts have been driven by semiconductors. However, if our index is to move higher to 10,000 points, it’s clear that semiconductors alone will not be enough. One of the standout stocks outside the semiconductor sector this year has been Hyundai Motor, which rose to third place in market capitalization rankings in early January, boosted by the unveiling of Boston Dynamics' humanoid robot, Atlas.

The industries positioned at the center of U.S. reshoring, such as shipbuilding and nuclear power, are also gaining attention. More broadly, given Korea’s strength in intermediate goods and manufacturing competitiveness, I believe we may be seeing a broader re-rating of Korea’s manufacturing sector as a whole.

Jason Lui, head of APAC equity and derivatives strategy at BNP Paribas

Lui: We do not have any official index forecasts, but in terms of catalysts, the ongoing product announcement of (sixth-generation high bandwidth memory) HBM4 products should help propel the high earnings growth expectations. The upcoming [FTSE World Government Bond Index] inclusion may also bring more foreign capital to the Korean government bonds, benefiting the overall capital market. Finally, pending the implementation of the Reshoring Investment Account scheme (offering capital gains tax exemptions for divesting from foreign markets and investing in local bourses), some of the domestic investors may replace their foreign holdings with domestic assets.

The Kospi has moved past 6,000 points. What was the main driver of the recent rally?

Kim: The fundamental driver behind this strong rally is the sharp upward revision in earnings expectations for listed Korean companies. At present, the market consensus projects that listed firms will generate around 560 trillion won ($391 billion) in operating profit by year-end. Just three months ago, that figure was closer to 300 trillion won, showing that profit expectations have nearly doubled — an encouraging development.

Whether the market is overheated ultimately comes down to valuation: how high stock prices are relative to earnings. If the rally is driven by semiconductors alone, I believe the index could still approach 7,000 points on the back of the rapid growth of the companies’ operating profit. If, in addition to semiconductors, other sectors post even modest gains, then reaching the 7,900-point level we have suggested would be achievable.

Whether the upward trend will continue in the long term depends not only on market momentum and flows, but also on policy-driven support. One of the first actions taken by the current government was to lay the groundwork for attracting long-term capital, including the amendment to the Commercial Act aimed at requiring the cancellation of treasury shares.

The Kospi delivered exceptional gains in 2025 and continues its bull run this year. Do you see this as a sustainable rally backed by structural improvements, or are we approaching overheated territory?

![Employees celebrate at the dealing room of Hana Bank’s headquarters in Jung District, central Seoul, on Feb. 25 after the Kospi closed above the 6,000 mark for the first time. [NEWS1]](https://koreaseafood.online/data/photo/2026/02/25/643db984-4f9e-41e1-a2ed-cd2fd1e88842.jpg)

Employees celebrate at the dealing room of Hana Bank’s headquarters in Jung District, central Seoul, on Feb. 25 after the Kospi closed above the 6,000 mark for the first time. [NEWS1]

Kim: The Kospi index has risen sharply in a short period of time. Last year, the index climbed 75 percent, and we’ve already reached roughly half of last year’s total gains. Achieving that in just two months suggests we can have even greater expectations going forward.

Whether this rally continues structurally would be closely tied to valuation. The so-called Korea discount exists partly because Korea’s key industries are highly cyclical. Of the roughly 560 trillion won that listed Korean companies are expected to earn this year, about half comes from semiconductor companies — the key cyclical industry. However, I believe we may be at a structural turning point. Unlike in the past, amid the AI revolution, expectations of prolonged supply shortages are building and could last for quite some time. So while cycles will still exist, if they become longer and more sustained, we may no longer need to view the industry as purely cyclical.

Lui: The rally in 2026 has largely been driven by the strong earnings per share (EPS) growth expectation as the Kospi 200 12-month forward EPS has been revised up by 43 percent since the start of the year. The strong earnings momentum is being supported by the extreme supply and demand imbalance in the semiconductor sector. Based on expected earnings over the next 12 months, the Kospi 200 index is still trading slightly below its long-term average price-to-earnings ratio. More importantly, foreign fund flows remain subdued relative to the magnitude of the outperformance of Korean equities, so there could be more room for foreign inflow.

Some raise concerns that the concentration of a narrow set of big caps driving the rally is an unhealthy signal. Do you agree with the view?

Kim: The current AI boom could generate many additional opportunities beyond a handful of players like chip giants as AI monetization broadens across the economy.

At this stage, hyperscalers are still in the early phase of investing in AI to make money, driving demand for memory chips. But when AI begins to generate substantial profits, value creation will likely extend beyond semiconductors into consumer goods, software and other industries.

In one possible scenario, households may eventually own multiple robots. If they become more prevalent than cars, then companies that design, manufacture, assemble and supply robots will all stand to profit. In another scenario, various software services like large language models may increasingly shift toward subscription-based models as AI improves productivity. Insurance, brokerage commissions and other financial services could also evolve, with costs declining and new platforms emerging as sources of influence and value.

![An electronic board at the dealing room of Woori Bank, central Seoul, shows the Kospi surging past the 6,000 level in a morning trading session on Feb. 25. [WOORI BANK]](https://koreaseafood.online/data/photo/2026/02/25/53a71757-4700-44b8-b1af-12d21a686b7a.jpg)

An electronic board at the dealing room of Woori Bank, central Seoul, shows the Kospi surging past the 6,000 level in a morning trading session on Feb. 25. [WOORI BANK]

Lui: The key tech companies have been the major driver of strong EPS growth expectations. Therefore, we could see a risk of correction if they cannot deliver on the elevated growth expectations. For the non-tech stocks, investors will also be looking for progress in corporate governance reform, such as the reduction in treasury shares.

How do you view the divergence between the Kospi and the won’s movements, where the won remains persistently weak against the dollar despite the Kospi being on a tear?

Kim: The dollar–won exchange rate at 1,400 has effectively become the new normal. A country’s currency reflects its fundamentals, and given Korea’s slowing growth rate and rising household debt, it is difficult to avoid a structurally weak won.

In the past, a 1,400 won exchange rate would have been associated with a much weaker environment — one in which the Kospi might have struggled to even hold 2,000 points. Yet, despite the recent strengthening of the won, the Kospi continues to rise day after day in the changed structural conditions.

Lui: We believe the won's weakness is largely due to the interest rate differentials and the persistent purchases of foreign assets by domestic investors. We are bullish on the won this year with an end-2026 forecast of 1,400 that reflects our expectation that the currency will outperform broad Asian currencies and appreciate against the U.S. dollar. As in other aging economies, the current surplus has been well-recycled into overseas investment — led by institutional and retail investors — sparking persistent won weakness in the last few years.

The Bank of Korea (BOK) has signaled the end of its rate cut cycle, and with the nomination of Kevin Warsh, the possibility of U.S. interest rate cuts is increasing. How do you anticipate future domestic and international interest rate movements, and how do you expect domestic and international indices to respond accordingly?

Kim: Hana Securities expects the Bank of Korea to cut its benchmark interest rate by 25 basis points once in the fourth quarter of this year due to the weak domestic economy. This is currently a minority view. While exports remain solid, domestic demand is sluggish. Therefore, concerns about the domestic economy could prompt a single rate cut. If rates are cut because the economy weakens, the stock market may experience short-term volatility. In Korea’s case, a rate cut would be driven by concerns over slowing domestic growth. However, exports remain strong, and the Korean stock market — including the Kospi — is closely tied to the export cycle. From that perspective, a rate cut could still be viewed positively for equities.

Lui: We still expect the Bank of Korea to hold the policy rate at 2.5 percent through to the end of 2027 in our base case. At this juncture, we see a high bar for either a rate cut or hike. We think the likelihood of the latter is higher than the former.

In the case of a cut, we think several conditions would need to be fulfilled for the BOK to consider cutting rates. It would need to see evidence of a continued and widening negative output gap. Also, the labor market would need to show further signs of deterioration alongside a sustained increase in the unemployment rate. There would need to be evidence that inflationary risks were contained, and that risks of further disinflation were increasing. Moreover, elevated financial stability risks from the weakness of the and a continued rise in Seoul metropolitan area housing prices may need to be contained.

As for a hike, we think inflation is key. If a positive shift in the output gap is associated with sharp increases in inflationary pressure, the BOK may seriously consider hiking rates, in our view. More specifically, several consecutive prints showing monthly year-to-year [consumer price index] inflation above 2.5 percent could quickly shift the central bank’s focus to inflation. We think rate hikes could come into play in this scenario, especially if they are supported by lingering financial stability concerns.

BY JIN MIN-JI, PARK EUN-JEE [[email protected]]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)