From trainers to trillions: Musinsa’s 10 trillion won IPO target sparks valuation debate

Published: 25 Sep. 2025, 07:00

-

- JIN MIN-JI

- [email protected]

![A Musinsa store in Seongsu-dong in eastern Seoul [MUSINSA]](https://koreaseafood.online/data/photo/2025/09/25/231b98f3-3583-4f40-9a6b-48356135c292.jpg)

A Musinsa store in Seongsu-dong in eastern Seoul [MUSINSA]

Musinsa, once a sneaker photo-sharing community, has grown into Korea’s leading fashion platform — and is now eyeing a public listing worth a whopping 10 trillion won ($7.2 billion) valuation.

That number is even higher than 4.8 trillion won valuation received by K-pop powerhouse HYBE when it went public in 2020. The targeted valuation would place Musinsa on par with Korea Aerospace Industries, which had a market cap of 10.6 trillion won, and just below Buldak ramyeon maker Samyang Foods, whose market cap was 11.2 trillion won as of Wednesday.

“Musinsa is aiming for a 10 trillion won market value before going public,” said a fashion industry insider, who spoke on the condition of anonymity. “It hasn’t finalized which exchange it will list on, but it’s open to several options, including ones in the United States.” The target is more than triple the 3.5 trillion won valuation it received in 2023.

In August, Musinsa — which is 52.35 percent owned by its founder and CEO Cho Man-ho — sent a request for proposal to investment banks to pitch for a role in managing the initial public offering (IPO). Its goal for the IPO is to secure funds to open more stores, both domestically and internationally.

Since its launch in 2001, Musinsa has become a must-visit destination for style-savvy tourists, and has come to be known for its affordable yet cutting-edge streetwear. It has become a prominent name in the industry that have been largely driven by conglomerates like Samsung C&T and LF. Korea's first-ever fashion unicorn, Musinsa now operates in 13 countries and globally attracts over 10.19 million monthly active users.

But despite the rapid growth backed by global investors like Sequoia Capital and KKR private equity, experts generally say the market valuation is bloated considering its current earnings.

![Displays on Musinsa platform [MUSINSA]](https://koreaseafood.online/data/photo/2025/09/25/bac378ff-0cb8-4554-821d-0b1c7f875b66.jpg)

Displays on Musinsa platform [MUSINSA]

Overvaluation, or untapped potential?

In the fiercely competitive industry, Musinsa has successfully transformed from a streetwear community into a leading style platform, expanding into beauty, sports and lifestyle — demonstrating its strength across both online and offline markets.

Its rapid growth has been fueled by strong streetwear sales, the launch of its in-house brand Musinsa Standard and lifestyle brand 29Edition, as well as the acquisition of rivals like 29CM.

Initially capturing the hearts of young men in their late teens to early 20s, Musinsa has since broadened its appeal to women as well as to those in their 30s and 40s with its minimalist and staple-driven style — a shift clearly reflected in its growing earnings.

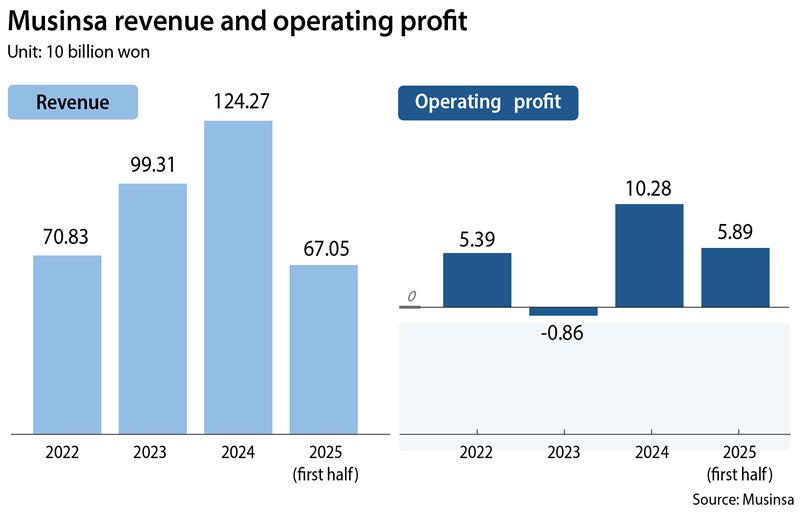

musinsa earnings

Musinsa reported 670.54 billion won in revenue in the first half the year, up 22 percent on-year. It logged 58.86 billion won in operating profit, up 23 percent on-year.

The figures are higher than some traditional fashion giants, like Shinsegae International, which reported 2.37 billion won in operating profit during the same period, down 90 percent due to inventory write-down costs, and Hyundai Home Shopping’s Handsome, which reported 22.52 billion won in operating profit, up 3.1 percent.

Despite its rapid growth and strong potential for further expansion, many believe Musinsa’s desired market valuation is overhyped.

“Based on last year’s net profit, its price-to-earnings (P/E) ratio stands at 143 times,” according to Oh Li-na, an analyst at LS Securities. “Even accounting for the second half being the peak season in the fashion industry, the ratio based on this year’s expected annual earnings remains above 100 times. This is unusually high — something that may be seen only in some coin companies — and is difficult to justify.”

The P/E ratio measures how much investors are willing to pay for each unit of a company’s earnings, with high ratio indicating possible overvaluation and the low ratio suggesting possible undervaluation of the company.

![Beauty products of Oddtype, Musinsa's store brand [MUSINSA]](https://koreaseafood.online/data/photo/2025/09/25/6100a2b8-3518-4c6c-80aa-f083b9bd83fd.jpg)

Beauty products of Oddtype, Musinsa's store brand [MUSINSA]

Aggressive expansion

To convince potential investors of its targeted 10 trillion won market valuation, Musinsa is aggressively expanding both domestically and globally to demonstrate strong growth momentum, as increased revenue can help a company secure a favorable valuation ahead of an IPO.

On top of offering an online Musinsa Global Store in the operating countries, the company established Musinsa Japan in 2021. It also formed a joint venture — Musinsa China — with Anta Sports, China’s largest sportswear company, in August. Japan and China are currently Musinsa’s most important overseas markets.

But its overseas performance remains minimal, with exports accounting for just 0.34 percent of its 1.24 trillion won revenue last year. The company attributed the weak export figure to the way commission revenue from partner brand sales on the Musinsa Global Store is calculated, as these transactions are classified as domestic.

Musinsa is also expanding domestically, launching cosmetics brands like Oddtype, and opening more stores.

Musinsa plans to operate 30 Musinsa Standard stores by the end of this year, up from 19 last year. In the first half of next year, it will also open its largest retail space to date — the so-called Musinsa Mega Store Seongsu — a 2,000-pyeong (6,611-square-meter) store that will offer fashion, beauty, footwear and food and beverage products.

The aggressive expansion and diversification of product categories reflects Musinsa’s broader strategy to boost revenue and enhance its overall market valuation.

Company valuation is typically assessed using metrics like the P/E ratio or price-to-sales ratio — the latter calculated as market capitalization divided by total revenue — which means that higher revenue can be advantageous for companies aiming to justify a higher valuation.

Though overpriced, Musinsa may still become Korea’s next member of the 10 trillion won club. If so, they would follow in the footsteps of Samyang Foods, whose stock has surged more than 15-fold over the past five years, and cosmetics company APR, who saw share prices jump more than three times within just a year and a half since its IPO in February last year.

“K-fashion isn’t visibly taking off overseas yet, but the market is pricing in the hope that Musinsa could follow a similar path to Samyang Foods and APR, whose shares skyrocketed,” said Seo Yong-gu, a professor of business at Sookmyung Women’s University.

BY JIN MIN-JI [[email protected]]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)