SK hynix set to overtake Samsung after posting record $33.1B profit in 2025

Published: 28 Jan. 2026, 18:31

Updated: 28 Jan. 2026, 18:32

-

- LEE JAE-LIM

- [email protected]

Audio report: written by reporters, read by AI

![SK hynix's Icheon headquarters in Gyeonggi on Oct. 29, 2025. [YONHAP]](https://koreaseafood.online/data/photo/2026/01/28/d6d73bd0-8ed9-4437-b24d-1a89348ac7ea.jpg)

SK hynix's Icheon headquarters in Gyeonggi on Oct. 29, 2025. [YONHAP]

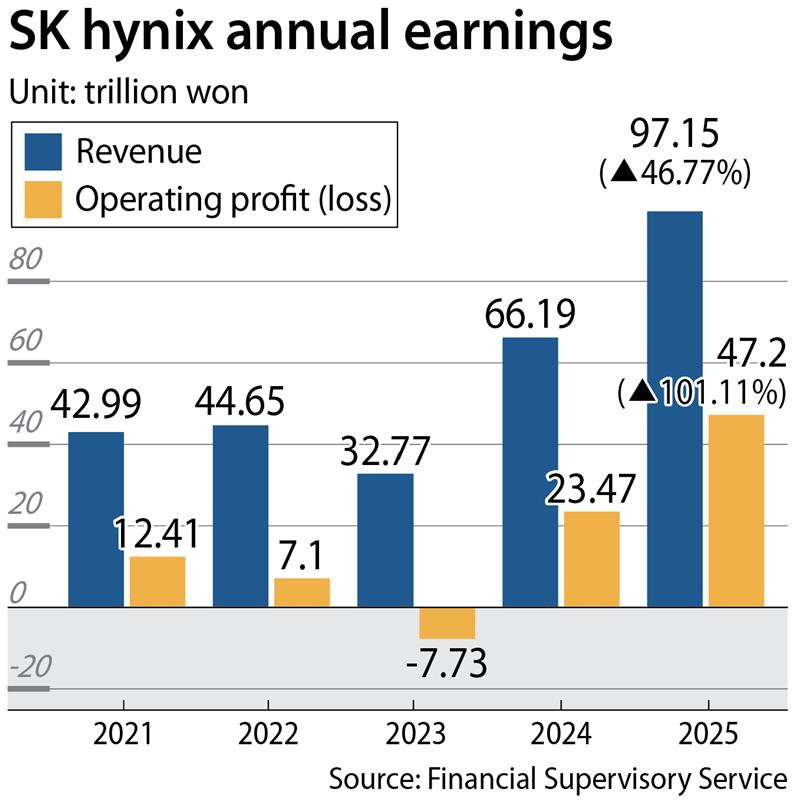

SK hynix posted an all-time high operating profit of 47.21 trillion won ($33.1 billion) in 2025, more than double the previous year's figure, as the company fully capitalized on an AI-driven memory supercycle that boosted demand and pricing power.

For the first time ever, the memory maker is set to overtake Samsung Electronics in operating profit, opening a gap of more than 3 trillion won after Samsung earlier this month forecast operating profit of 43.53 trillion won.

SK hynix's operating profit exceeded the market consensus of 44.5 trillion won compiled by FnGuide. Revenue for 2025 reached 97.15 trillion won, up 46.77 percent on year and above the market forecast of 95.3 trillion won. Net profit came in at 42.95 trillion won, surging 116.92 percent on year and topping analysts’ expectations of 40.67 trillion won.

Fourth-quarter operating profit jumped 137.2 percent on year to 19.17 trillion won, surpassing the market forecast of 16.46 trillion won. Quarterly revenue rose 66.1 percent to 32.83 trillion won, exceeding the consensus estimate of 31 trillion won, while net profit increased 90.4 percent to 15.25 trillion won, broadly in line with market expectations.

The company said revenue from high bandwidth memory (HBM) more than doubled from the previous year, contributing significantly to its record performance. SK hynix expects the role of memory semiconductors to become increasingly critical in the AI era, as industry focus shifts from training to inference models and as supporting infrastructure, such as data centers, continues to expand.

“Demand is expected to grow not only for high-performance memory such as HBM, but also across the broader memory portfolio, including server dynamic random access memory [DRAM] and NAND,” the company said in a statement.

To meet robust demand, SK hynix plans to accelerate the completion of its M15X fab in Cheongju, North Chungcheong, which is scheduled to begin trial operations next month. The company is also constructing the first of four fabs at its Yongin semiconductor cluster in Gyeonggi, slated to start production next year, and is building advanced packaging facilities in Cheongju and Indiana.

SK hynix’s global HBM market share stood at 57 percent in the third quarter of 2025, according to Counterpoint Research, more than double Samsung Electronics' 22 percent.

A key determinant of market share and profitability going forward — and a focal point of competition between SK hynix and Samsung — is the allocation of HBM4 supply for Nvidia’s next-generation Vera Rubin processors. Multiple local media reports indicate that SK hynix has already secured nearly 70 percent of Nvidia’s total HBM4 supply, well above market expectations of around 50 percent.

SK hynix is also reportedly considering establishing a U.S.-based entity to oversee AI investments for SK Group, which would assume control of approximately 10 trillion won in overseas AI-related assets currently held by group affiliates, according to an exclusive report by Maeil Business Newspaper.

The company’s shares closed at a record high of 841,000 won on Wednesday, up 5.13 percent from the previous session. Market capitalization reached 612 trillion won on the day. After the market closed, SK hynix announced the cancellation of 15.3 million treasury shares worth 12.2 trillion won, equivalent to 2.1 percent of outstanding shares, to enhance per-share value and shareholder returns.

Analysts expect memory supply tightness to persist through 2027, as Big Tech companies race to secure AI leadership, further fueled by the rise of physical AI applications such as humanoid robots and autonomous driving.

SK Securities raised its target share price for SK hynix to a record 1.5 million won from 1 million won, citing a structural expansion in memory valuation rather than a cyclical peak. KB Securities also increased its target price from 950,000 won to 1.2 million won.

According to KB Securities researcher Kim Dong-won, the upward revision reflects surging DRAM and NAND prices, leading to higher operating profit forecasts of 132 trillion won for 2026 and 151 trillion won for 2027.

BY LEE JAE-LIM [[email protected]]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)