Insurance firms launch new mental health products as demand continues to rise

Published: 09 Apr. 2026, 07:00

Audio report: written by reporters, read by AI

![Two people stand outside the Gwanghwamun Kyobo Life Building in Jung District, central Seoul on Dec. 1, 2025. [YONHAP]](https://koreaseafood.online/data/photo/2026/04/09/23b954ae-57b0-41cc-8bd3-619ce21eced8.jpg)

Two people stand outside the Gwanghwamun Kyobo Life Building in Jung District, central Seoul on Dec. 1, 2025. [YONHAP]

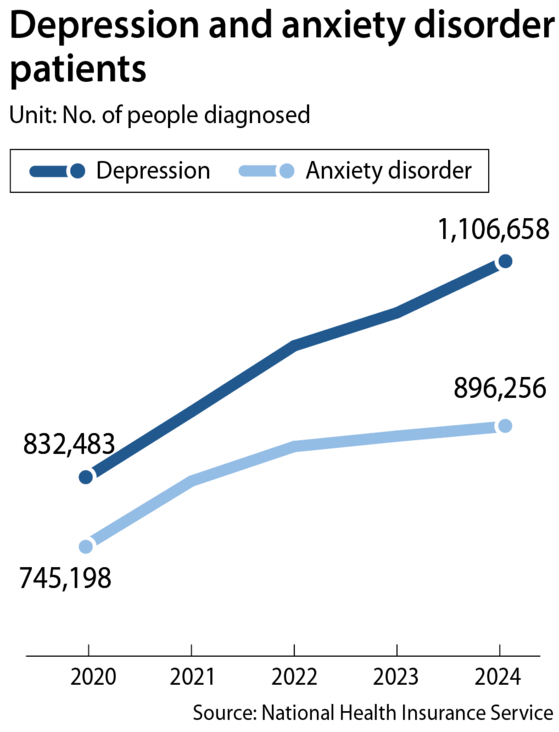

The number of people in Korea focusing on their mental health is rising. In response, insurance firms are rapidly launching new products that cover mental illness.

Coverage is also diversifying beyond depression to include panic disorder and eating disorders.

Kyobo Lifeplanet Life Insurance recently launched a separate insurance product for panic disorder and burnout. The policyholder, in the case of a 30-year-old woman, would pay a one-time premium of less than 4,000 won ($2.66). If she is diagnosed with the relevant condition within a year after the payment, a one-time payout of 100,000 won will be provided to the policyholder.

The burnout policy is designed to pay out if the insured is definitively diagnosed with a depressive episode. A depressive episode refers to a condition in which depressive symptoms continue for at least two weeks. Typical symptoms include feelings of emptiness, lethargy, chronic fatigue and changes in sleep and appetite.

Hanwha Insurance introduced a rider for its women’s insurance product that covers examination fees and hospitalization costs for sleep disorders and eating disorders caused by stress.

![An AI-generated illustration about insurance products that covers mental health [CHATGPT]](https://koreaseafood.online/data/photo/2026/04/09/38ef835b-0fe4-4435-85f0-e7c496b4443d.jpg)

An AI-generated illustration about insurance products that covers mental health [CHATGPT]

Children’s insurance is also being designed with increasing focus on mental health.

Diagnostic coverage for conditions such as attention deficit hyperactivity disorder and post-traumatic stress disorder, which children may experience as they grow, is being offered by Hyundai Marine & Fire Insurance, Meritz Fire & Marine Insurance and Samsung Fire & Marine Insurance.

Depending on the rider, treatment costs for schizophrenia, obsessive compulsive disorder and panic disorder may also be covered. Indemnity health insurance policies purchased after 2016 also cover insured treatment costs for major mental illnesses.

Insurers have moved to develop such products as mental health has recently emerged as a major social issue.

“Deteriorating mental health is leading to a range of social problems, including delayed employment, career interruptions and lower labor productivity,” Kim Kyung-sun, a research fellow at the Korea Insurance Research Institute, said. “Insurers need to develop products and provide preventive services to promote mental health and respond to consumer demand.”

A limitation is that most insurers’ mental health-related products still stop at diagnosis benefits.

The industry says there is not yet enough accumulated policyholder data to actively extend coverage to treatment costs or hospitalization expenses.

“Because mental illnesses are difficult to cure completely, treatment and hospitalization can be prolonged, which makes it hard to measure loss ratios precisely,” an insurance industry representative said.

“It is also true that there are concerns about moral hazard because it is difficult to verify whether a policyholder had an untreated mental illness at the time of enrollment if that was not disclosed.”

Diagnoses can vary depending on a physician’s subjective judgment, and conflicts may also arise between insurers and policyholders in the process of proving whether a claim is justified.

In fact, DB Insurance’s Mental Care Health Insurance, which drew attention last year for covering hospitalization and outpatient expenses across a broad range of illnesses, is currently off the market temporarily while it undergoes reorganization.

Even so, experts say an expansion of coverage through public and private insurance is inevitable as consumer demand for mental health-related coverage grows.

“For some mild mental illnesses, public health insurance coverage is limited, making it difficult to receive needed treatment, and even for severe patients, public insurance support has limits during long-term hospitalization, so the scope of coverage remains restricted,” Kim said.

“The public and private sectors need to work closely together.”

Diversifying insurance products tailored to specific groups — such as people in their teens and 20s — to make up for the lack of statistical data and having insurers provide mental health management programs alongside their products are also cited as alternatives.

BY OH HYO-JEONG [[email protected]]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)