Korea could slip into another currency crisis without larger foreign reserves, economist warns

As the won hovers near 1,500 per dollar, some experts are urging the central bank to sharply raise its greenback holdings to guard against future turmoil.

Two people in a tug of war for the dollarGETTY IMAGES PRO

[NEWS ANALYSIS]

The won's persistent weakness against the dollar is raising calls for Korea to build up its foreign exchange reserves, with some economists arguing that the country's holdings are too small relative to the vulnerability of the currency. Some have even warned that maintaining the current level while pursuing expansionary fiscal policies could leave Korea exposed to another currency crisis.

While the won fell slightly below the psychologically important 1,500-per-dollar mark on Wednesday for the first time since May 29, the currency remains under pressure, down nearly 4 percent from the start of the year.

GoogleAdmanager-KJD

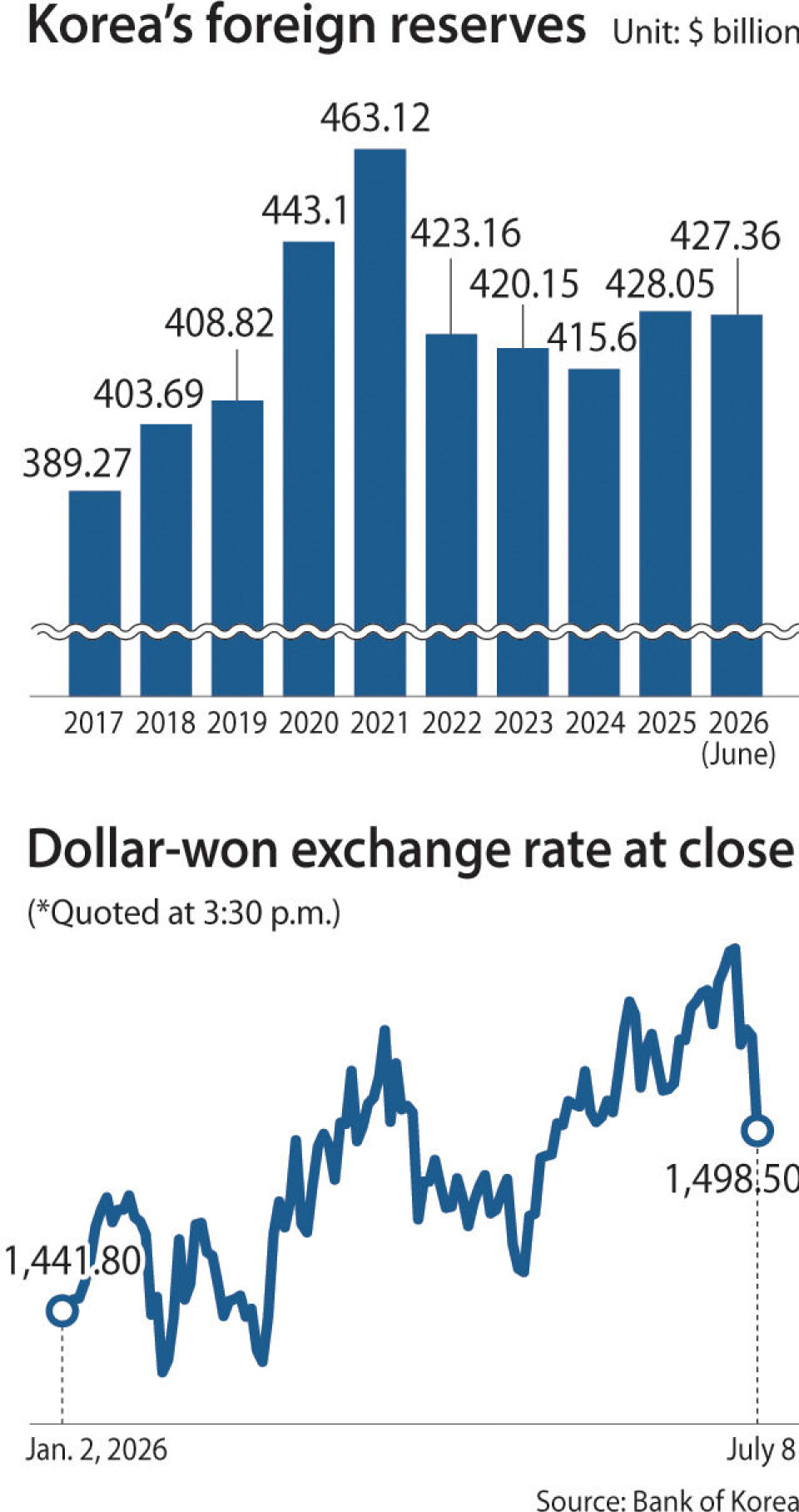

The weakness has incited calls for Korea to up its foreign reserves, as they serve as a key buffer for the Bank of Korea (BOK), allowing it to intervene in currency markets during periods of excessive volatility. The foreign reserves stood at $427.36 billion in June, the world's 13th largest. The ranking has continuously declined from 9th in December 2025.

"If Korea's foreign exchange reserves remain at the current level as fiscal spending expands and government debt rises, the country could slip faster into another foreign exchange crisis," Kim Dae-jong, a business professor at Sejong University, warned. He has repeatedly said insufficient foreign reserves will push the Korean economy into another currency crisis, with estimates that the country needs roughly $700 billion in foreign exchange reserves based on his assessment of reserve adequacy using International Monetary Fund (IMF) metrics.

Korea's foreign reserves fell below the IMF’s recommended adequacy threshold in 2022, with the country's reserve buffer standing at 97 percent of the level recommended by the IMF's Assessing Reserve Adequacy metric for emerging markets. The IMF considers a ratio of 100 percent to 150 percent to be adequate.

The IMF stopped tracking Korea's adequacy in 2023. However, Korea's average foreign reserves in 2022 stood at $423.16 billion, only slightly below the current holdings.

More the merrier

Despite a record trade surplus fueled by an AI-driven export boom, the won has remained stubbornly weak against the dollar. The currency has fallen 3.9 percent against the greenback this year as foreign investors’ mass selling of Korean equities — a net 149.05 trillion won in the first half, the largest on record for the period — has weighed on the won.

“Given Korea’s heavy reliance on exports and its lack of a currency swap line with the United States, the country is particularly vulnerable in terms of reserve adequacy. If exports and imports are disrupted, the exchange rate rises and creates currency risks,” said Prof. Kim. “Foreign exchange reserves are a safety buffer, but ours are only about 22 percent of [last year’s] GDP — far lower than other regions like Taiwan.”

Taiwan, the world’s sixth-largest holder of foreign exchange reserves and a fellow export-driven economy, holds reserves equivalent to about 70 percent of its GDP, while Hong Kong — the 10th-largest holder — has reserves exceeding 100 percent of its GDP.

Global economists agree that Korea needs to build up more foreign reserves.

“The BOK should rebuild FX reserves once net equity flows become positive,” said Chandresh Jain, the director of emerging markets rates and FX strategist at BNP Paribas, noting the reserves the BOK has lost by intervening in the market in a bid to stop depreciation over the last few months.

“The higher, the better,” Jain noted.

The central bank net sold $13.63 billion worth of its reserves in the first quarter to tame the currency, net selling for the sixth straight quarter since the last quarter of 2024.

“High FX reserves are particularly valuable when a currency is under depreciation pressure,” Jain said, but added that “it has to be navigated properly and shouldn’t push the currency weaker during the process,” as a BOK buying spree of dollars will further depreciate the already weak won.

Not the ultimate solution

Despite the strong arguments, not every economist agrees. In fact, some say there are opportunity costs with higher reserves.

“Foreign reserves are largely held in highly liquid assets such as U.S. Treasurys, offering relatively low returns,” said Huh In, an economics professor at the Catholic University of Korea. “Holding onto dollars from record trade surpluses simply as a buffer against market volatility comes with a significant opportunity cost.”

The BOK does not disclose the return rate on its foreign reserves, but local media have estimated the average annual return at around 4 percent.

Prof. Huh cited Japan as evidence that larger reserves do not necessarily lead to better currency management. Japan was the second-largest holder of foreign reserves with $1.31 trillion as of the end of May, but the yen has been depreciating sharply, dropping to a 40-year low against the dollar this month to hit its weakest level since 1986.

Foreign exchange traders in Hana Bank's trading room in central Seoul on July 8. The won slipped below 1,500 per dollar for the first time since May 29.YONHAP

A more bearish view argues that the size of Korea’s foreign reserves has little bearing on the exchange rate, making a further buildup unnecessary.

If reserves were unreasonably low, increasing them would be necessary, but that isn’t the case today as the won’s weakness reflects the broad strength of the dollar triggered by the rate differential between Korea and the United States, according to Park Seok-hyun, the deputy head of the wealth management products division at Woori Bank.

“The won's weakness should ease once concerns that the U.S. Federal Reserve may raise interest rates sooner than expected subside,” Park said.

The Korea-U.S. interest rate differential has remained inverted for a record three years and 11 months, since July 2022, apart from a brief interruption in August 2022 when the gap temporarily closed.

A more fundamental way to stabilize the won would be to create incentives for foreign investors to hold the currency over the long term.

“Korea has extended foreign exchange trading around the clock, but the won is still not freely traded offshore — reducing foreign investors’ incentives to hold won over the long term,” said Kim Han-soo, a senior research fellow at the Korea Capital Market Institute.

“As a result, investors use the currency primarily for transactions, potentially making it more susceptible to one-way flows during periods of market stress. The next step [to stabilizing the won] should be to gradually allow offshore trading so foreign investors have greater reason to hold the won over a longer horizon.”

Korea's finance ministry plans to implement an offshore won settlement system in January next year.